Registering a small company in Poland does not automatically make it eligible for public funding. A business may satisfy the general definition of a small or medium-sized enterprise and still fail the conditions of a specific grant call because of its ownership structure, sector, location, financial condition, project type, budget or previous public aid.

This is why grant eligibility should never be treated as a single yes-or-no question.

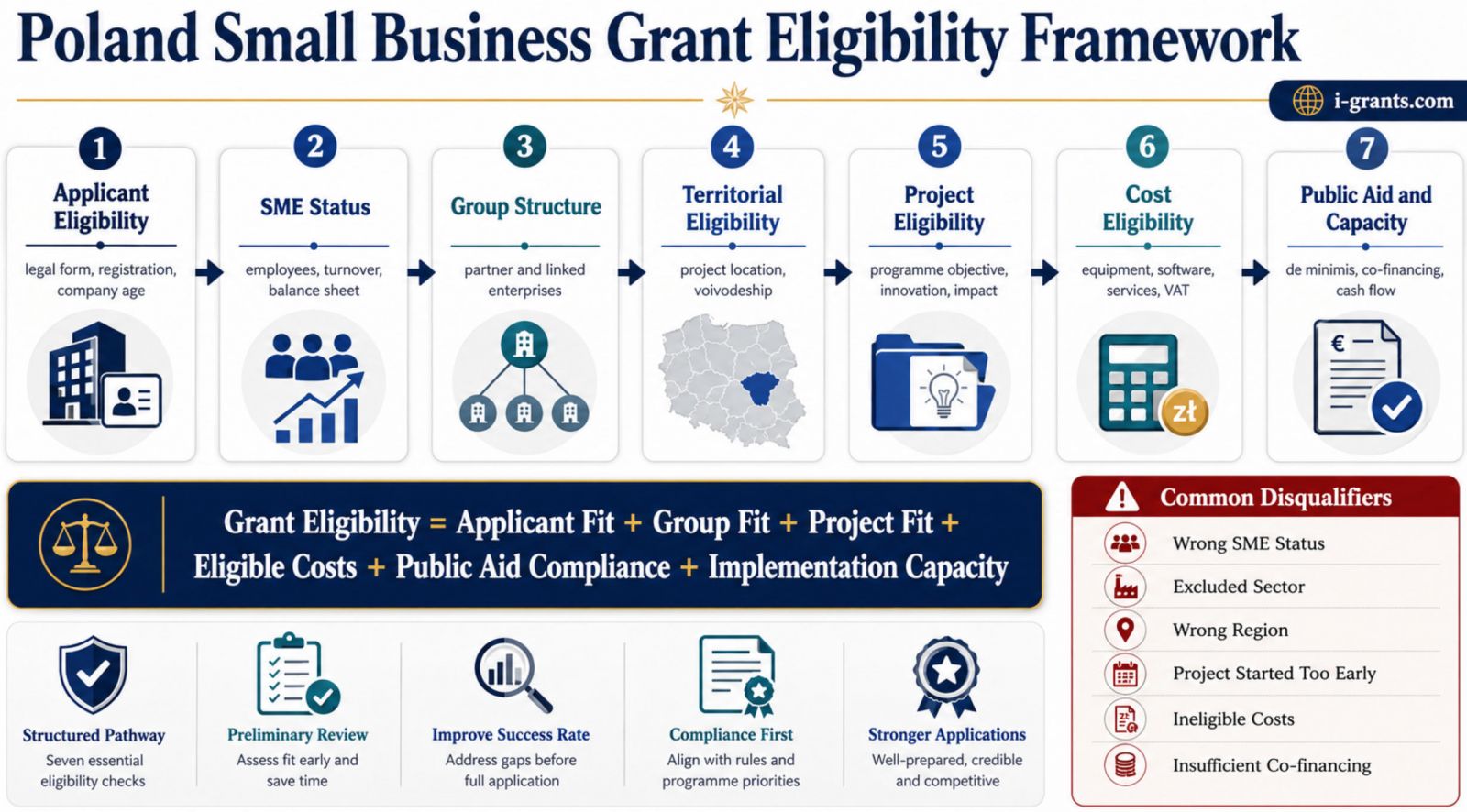

A Polish business grant usually involves several separate tests. The programme may examine whether the applicant has the correct legal status, whether the wider enterprise group remains within the SME thresholds, whether the project will be implemented in an eligible region, whether the proposed activities match the purpose of the call, whether the costs can be financed and whether the requested aid complies with European public aid rules.

Passing one test does not guarantee success in the others.

A company may be an eligible SME but propose an ineligible project. The project may fit the call, but the planned equipment may not be an eligible cost. The budget may be acceptable, but the company may have already used its available de minimis aid. A foreign-owned company may be legally established in Poland, but the project may not meet the required territorial or operational conditions.

The most useful eligibility question is therefore not simply, “Is this a small business?” It is:

Do the applicant, enterprise group, project, location, costs, financing structure and public aid position all satisfy the rules of the same call?

This guide explains how that assessment works and why many otherwise promising applications fail before evaluators consider the quality of the business idea.

Eligibility Is a Chain of Separate Tests

Eligibility begins with the applicant, but it does not end there.

A typical Polish grant call may examine seven connected levels. The first is the organisation itself: its legal form, registration, age, sector and business activity. The second is the wider enterprise group, including partner and linked companies. The third is the place where the investment or activity will be implemented. The fourth is the nature of the project. The fifth is the proposed budget. The sixth is the applicable public aid regime. The seventh is the company’s capacity to finance and implement the project.

This structure explains why apparently similar companies can receive different eligibility results. A manufacturing company may qualify for a regional equipment programme but not for an R&D competition. A software company may fit a digitalisation call but fail because the project began before the application date. A young company may qualify for an accelerator instrument but be too new for a programme requiring several completed financial years.

Eligibility is always call-specific.

General rules, such as the European SME definition, provide the starting framework. The binding answer comes from the regulations, criteria and annexes of the individual call.

Does the Company Meet the EU SME Definition?

Most Polish programmes financed through European funds use the EU definition of micro, small and medium-sized enterprises.

The definition considers the number of employees and financial size. To qualify as an SME, an enterprise must employ fewer than 250 people and remain within the relevant turnover or balance sheet threshold.

Table 1. EU SME Size Thresholds Used in Polish Grant Programmes

| Enterprise category | Employees | Annual turnover | Annual balance sheet total |

|---|---|---|---|

| Microenterprise | Fewer than 10 | Up to EUR 2 million | Up to EUR 2 million |

| Small enterprise | Fewer than 50 | Up to EUR 10 million | Up to EUR 10 million |

| Medium-sized enterprise | Fewer than 250 | Up to EUR 50 million | Up to EUR 43 million |

The employee threshold must be satisfied. For the financial criterion, the enterprise generally considers annual turnover or the annual balance sheet total.

However, a company cannot always calculate its size using only its own payroll and accounts. Ownership and control relationships may require the data of other entities to be included.

This is one of the most common sources of incorrect SME declarations.

A company with 20 employees may appear to be a small enterprise. If it is controlled by a much larger group, its figures may need to be combined with those of related entities. The resulting calculation may classify it as a medium-sized enterprise or remove it from the SME category entirely.

This matters because some Polish calls are reserved for micro and small enterprises, while others admit the full SME category. The maximum funding rate may also differ according to enterprise size.

Independent, Partner, and Linked Enterprises

The European SME rules distinguish between autonomous, partner and linked enterprises.

An autonomous enterprise generally has no significant ownership or control relationship that requires another company’s figures to be included. A partner enterprise usually involves a substantial ownership link without full control. A linked enterprise involves stronger control, such as a majority of voting rights or the power to appoint management.

The calculation can become more complicated when ownership passes through several companies or when the connection exists through individuals.

An applicant should examine:

-

Shareholdings between the applicant and other organisations.

-

Voting rights and the ability to appoint or remove management.

-

Contractual or factual control over another enterprise.

-

Parent companies, subsidiaries and indirect ownership chains.

-

Common individual owners operating in the same or adjacent markets.

-

Relationships with public bodies, universities or other institutions that may affect autonomy.

These relationships can change the data used for employee numbers, turnover and balance sheet totals.

The key principle is economic reality. Formal legal separation does not always mean that two businesses are treated as independent for SME or public aid purposes.

Poland’s PARP provides an SME qualification tool that can support a preliminary assessment. It is useful for identifying possible relationships and gathering the required figures. It should not be treated as a replacement for reviewing the ownership structure, official guidance and the declaration required by the specific programme.

For companies with complex ownership, foreign shareholders, investment funds or several related operating companies, an incorrect SME calculation can create serious risk. If the mistake is discovered after approval, the applicant may lose the grant or face recovery of funds.

SME Status Can Be Checked More Than Once

The applicant normally declares its SME status when submitting the application. The programme operator may verify it during assessment, before signing the funding agreement, during project implementation or during an audit.

Changes in ownership can also trigger renewed scrutiny.

For example, a company may qualify as a small enterprise when it applies but later become part of a larger group. Whether and when this affects the grant depends on the applicable SME rules, accounting periods, ownership change and programme documentation.

Natural business growth does not necessarily change the category immediately. EU rules contain mechanisms for assessing data across accounting periods. However, applicants should not assume that the original status remains valid regardless of later events.

A company planning a merger, acquisition, investment round or transfer of shares should examine the potential effect on its SME classification before signing the transaction, particularly when an application or funded project is active.

Who Counts as an Enterprise?

For public aid purposes, the concept of an enterprise is broader than a conventional commercial company.

The main question is whether the entity carries out an economic activity by offering goods or services on a market. Its legal form or method of financing may not be decisive.

Depending on the programme, an enterprise may therefore include a sole trader, limited liability company, joint-stock company, cooperative, social enterprise or a non-profit organisation carrying out economic activity.

This does not mean that every entity conducting economic activity may apply to every grant.

A programme may restrict applicants to companies registered in CEIDG or KRS, enterprises operating for a minimum period, startups below a specified age, firms from a particular sector or organisations selected through an intermediary.

Two concepts must be kept separate:

Enterprise under public aid law describes an entity carrying out economic activity.

Eligible applicant under a call describes an entity that satisfies the specific application rules.

An organisation can be an enterprise for public aid purposes and still be excluded from the call.

Legal Form, Registration, and Company Age

Many Polish business programmes require the applicant to be legally established and conducting economic activity in Poland. The exact requirement depends on the call.

Some competitions are open only to entities registered in the Polish business registers. Others focus on projects implemented in Poland and may contain additional conditions for foreign-owned companies.

Company age can also be decisive.

A startup programme may accept only companies established within a specified number of years. Another instrument may require completed financial statements or evidence of commercial activity, making very young companies practically or formally ineligible.

A company can therefore be too young for one call and too old for another.

Foreign-owned businesses should verify:

-

Whether a Polish legal entity is required.

-

Whether the applicant conducts real economic activity in Poland.

-

Where the project and funded activity will be implemented.

-

Which entity will incur and pay the project costs.

-

Where the financed assets and jobs will be located.

-

Whether the call requires a minimum operating or financial history.

Foreign ownership is not automatically a disqualifier. The relevant issues are usually the legal applicant, economic activity, project location, ownership relationships and compliance with the call.

An applicant should also check whether the Polish company has the authority and resources to implement the project independently. A newly created subsidiary with no employees, revenue or operating capacity may face difficulty proving that it can deliver a complex investment even if it is formally eligible.

Project Location Can Determine Eligibility

The registered office of the company and the place of project implementation are not always the same.

For regional funding, the decisive location may be where equipment is installed, jobs are created, research is conducted, production takes place or project results are used. The programme may also require financed assets to remain in the eligible region for a specified sustainability period.

A company registered in Warsaw may potentially apply under another region’s programme if the funded investment is genuinely implemented there. The exact answer depends on the call.

Location is particularly important for programmes covering Eastern Poland, individual voivodeships, rural areas, selected urban territories and regions with different levels of investment aid.

Applicants with several branches should identify which location will receive the funding and which entity unit will carry out the project. A vague statement that the company “operates across Poland” is not enough when the programme requires a specific implementation site.

Sector Eligibility Is More Complex Than a Business Code

Some programmes are open to a wide range of industries. Others prioritise or restrict support according to sector.

Three different situations are common.

A broadly open call may admit most business activities except those expressly excluded by public aid or programme rules.

A priority-based call may allow many sectors but award additional points to projects connected with regional smart specialisations, strategic technologies or selected value chains.

A closed sectoral call may accept only businesses from a defined industry, such as tourism, culture, energy, healthcare or manufacturing.

The company’s registered activity code may be relevant, but it may not be sufficient. A programme operator can ask for invoices, contracts, revenue history or evidence that the applicant genuinely operates in the required sector.

A company that recently added an activity code only to access a grant may fail if it cannot show real business activity.

Sector exclusions can also come from EU public aid rules. Certain agricultural, fisheries, coal, transport or financial activities may face special conditions or exclusions depending on the aid scheme.

The applicant must therefore check both the programme’s target sector and the legal aid basis.

Public Aid and the De Minimis Limit

Most grants to businesses are forms of public aid. This means that funding must comply not only with the programme rules but also with EU competition law.

One common form is de minimis aid. Since 1 January 2024, the general ceiling is EUR 300,000 per single undertaking over a rolling three-year period.

The phrase “single undertaking” is crucial.

The limit may apply not only to the applicant company but to several linked entities treated as one economic unit. A company cannot avoid the ceiling by distributing aid among several closely controlled businesses.

The EUR 300,000 ceiling also does not mean that every eligible company has a right to receive that amount. It is the maximum permitted under the general de minimis regime. The individual call may offer much less.

Table 2. Main Eligibility Checks Related to Public Aid

| Check | What the applicant must establish | Why it matters |

|---|---|---|

| SME status | Correct enterprise size after partner and linked companies are included | Some calls are limited to SMEs or particular SME categories |

| Single undertaking | Which connected entities must be counted together | De minimis limits may apply to the entire economic group |

| Previous public aid | Aid already received during the relevant period | The remaining available ceiling may be reduced |

| Aid intensity | Maximum percentage of eligible costs that can be funded | Determines the required own contribution |

| Cumulation | Whether several aid sources finance the same costs | Double financing or excessive aid may be prohibited |

| Recovery order | Whether the company must repay unlawful aid | Can prevent new public support |

| Undertaking in difficulty | Whether the applicant meets financial distress criteria | Many aid schemes exclude such enterprises |

Applicants should obtain and review records of previous de minimis aid and other public support. Poland’s SUDOP system can be used to check information about aid granted to businesses.

Public aid history should be analysed before the budget is finalised. Discovering at the end of preparation that the company has insufficient de minimis capacity can make the proposed financing structure impossible.

Another important issue is cumulation. A company may receive support from several sources, but it cannot necessarily use them to finance the same eligible cost beyond the permitted aid intensity.

For example, a regional grant, tax relief and other public support may need to be assessed together if they cover the same investment.

Undertakings in Financial Difficulty

Many grant schemes exclude undertakings in difficulty under EU public aid rules.

This concept is more technical than a temporary decline in profit. A company is not automatically “in difficulty” simply because it had a weak quarter or a single loss-making year.

The legal assessment may consider loss of subscribed capital, insolvency proceedings, eligibility for collective insolvency procedures, rescue or restructuring aid and, for some companies, specified debt and interest coverage indicators.

The precise test depends on the company’s legal form, size, age and the public aid basis used by the programme.

For this reason, applicants should not rely on a simplified online checklist. They should examine the call documentation and, where necessary, obtain financial or legal advice.

Grant operators may require approved financial statements, current management accounts or declarations confirming that the applicant is not an undertaking in difficulty.

A company that is formally eligible as an SME may still be excluded because of its financial condition.

Tax Compliance, Social Insurance, and Recovery Orders

Programme documentation often requires the applicant to confirm that it has no disqualifying tax or social insurance arrears, is not subject to insolvency restrictions and is not required to repay unlawful public aid.

Typical compliance checks include:

-

Tax liabilities and arrangements with the tax authority.

-

Social insurance liabilities to ZUS.

-

Insolvency, liquidation or restructuring status.

-

Recovery orders concerning unlawful state aid.

-

Criminal, professional or procurement-related exclusions.

-

Accuracy of declarations made in previous funding applications.

Not every temporary liability automatically leads to final rejection. Some calls may allow an approved payment arrangement, deferral or evidence that the issue has been resolved.

The exact wording of the criterion is decisive.

Applicants should not wait until the final week before submission to obtain certificates or clarify arrears. Even when a document is not mandatory at application stage, the underlying condition may still be checked before the funding agreement is signed.

False or incomplete declarations create a greater risk than a properly disclosed issue. They can lead to rejection, termination of the agreement or repayment of funds.

An Eligible Applicant Can Still Have an Ineligible Project

Passing the company-level tests does not mean the project is suitable.

Each call has a defined objective. A project must contribute to that objective in a convincing and measurable way.

An ordinary expansion project should not be described as research and development unless it contains real technical uncertainty and a structured research process. A standard software purchase should not be presented as digital transformation without explaining how it changes operations, productivity, security or data management.

The project must usually demonstrate a clear need, defined activities, realistic timetable, measurable outputs and a logical connection between the problem and proposed investment.

Some programmes also require innovation at a specified level, such as innovation within the company, region, country or international market.

A business can therefore satisfy all applicant conditions and still fail because its project is too ordinary, insufficiently developed or unrelated to the call.

Eligible Costs Are a Separate Test

Even when the applicant and project are eligible, individual budget items may not be.

Eligible costs must usually be connected to the project, necessary, reasonable, incurred within the permitted period, properly documented and compliant with procurement rules.

Potentially eligible categories may include:

-

Machinery and production equipment.

-

Software, licences and other intangible assets.

-

Construction, adaptation or installation works.

-

Research staff and contracted research services.

-

Specialist consulting, technical or certification services.

-

Training, promotion or internationalisation activities.

This does not mean that every programme finances all these categories.

Machinery may be central to an investment grant but unsuitable as the main cost of a research call. Consulting may be eligible only when directly connected to the funded activity. Promotion may be permitted in an export programme but excluded from a technology investment.

Working capital, routine operating expenses, used equipment, passenger vehicles, recoverable VAT, land, real estate or costs incurred before the eligible period may be excluded or restricted.

Applicants should build the budget from the call’s eligible cost rules, not from the company’s preferred shopping list.

Table 3. Applicant, Project, and Cost Eligibility Are Separate Tests

| Eligibility level | Main question | Typical reason for failure |

|---|---|---|

| Applicant eligibility | Is this organisation allowed to apply? | Wrong size, legal form, sector or company age |

| Group eligibility | Does the enterprise remain an SME after links are counted? | Related companies push it above the threshold |

| Territorial eligibility | Is the project implemented in an eligible location? | Investment is assigned to the wrong region |

| Project eligibility | Does the project match the purpose of the call? | Ordinary expansion is presented as innovation |

| Cost eligibility | Can the programme finance the proposed budget items? | Ineligible equipment, VAT, working capital or early expenses |

| Aid eligibility | Can support legally be granted at the requested level? | De minimis limit, cumulation or aid intensity issue |

| Capacity eligibility | Can the company finance and implement the project? | Insufficient cash flow, staff or own contribution |

This separation is one of the most important principles in grant preparation. A positive answer at one level does not correct a failure at another.

VAT, Own Contribution, and Cash Flow

VAT treatment must be checked against the current programme rules and the applicant’s legal ability to recover the tax.

It is unsafe to assume that VAT is always eligible or always excluded.

The result can depend on the total project value, the funding source, the applicant’s tax status and whether VAT can be recovered under national law.

The own contribution also involves more than inserting a percentage into the budget.

The company must be able to finance its required share, cover all ineligible costs, manage VAT if it is not funded and absorb payment delays.

Many programmes reimburse expenditure after the company has paid suppliers. Even when advance payments are possible, the applicant may need substantial working capital.

A company can therefore be formally eligible but financially unprepared.

The operator may assess financial statements, forecasts, credit capacity, investor commitments or bank financing. An unrealistic financing plan can weaken the application or prevent signature of the grant agreement.

Do Not Start the Project Too Early

Beginning the investment before the permitted date is one of the most serious eligibility risks.

Under public aid rules, the project may need to demonstrate an incentive effect. This generally means that the application must be submitted before the applicant makes an irreversible commitment to begin the investment.

The start of work may occur earlier than the company expects. It can include a binding equipment order, construction agreement or other commitment that makes the project difficult to reverse.

Before the rules are checked, the applicant should avoid:

-

Signing a binding supply or construction agreement.

-

Placing an irreversible equipment order.

-

Starting construction or installation works.

-

Paying a non-refundable deposit.

-

Beginning funded research activities.

-

Selecting suppliers in breach of applicable procurement rules.

Preparatory activities may be treated differently, but the exact definition must come from the call and applicable aid scheme.

An applicant should not assume that signing a contract is harmless because no invoice has yet been paid. The legal commitment itself may be enough to establish that the project has started.

A premature start can make the entire investment ineligible, not only the early cost.

Procurement Rules Can Affect Cost Eligibility

Receiving a grant does not always allow the beneficiary to choose any preferred supplier.

Depending on the programme, purchase value and applicant status, the project may be subject to public procurement law, the competitiveness principle, internal selection procedures, conflict-of-interest rules or publication in the Polish Competitiveness Database.

A cost can be eligible in nature but become non-reimbursable because the supplier was selected incorrectly.

This risk is particularly important when the applicant already has a preferred supplier or works with a related company. The procurement route should be checked before quotations are requested or agreements are signed.

Errors during procurement can lead to financial corrections, reduction of the grant or refusal to reimburse the expenditure.

Eligibility Is Not the Same as Competitiveness

Formal eligibility only allows the application to enter the competition.

It does not mean that the project will receive funding.

A competitive project normally needs more than compliance. It requires strong project logic, measurable outcomes, credible market evidence, a realistic budget, an experienced team and clear alignment with the evaluation criteria.

A company may pass every formal eligibility test and still receive a low score because the project is weak, poorly evidenced or insufficiently prepared.

This distinction is essential:

Eligible means the application is allowed to compete.

Competitive means the application has enough quality to win.

Applicants should not interpret an eligibility confirmation as a prediction of success.

The strongest eligibility review therefore also identifies readiness gaps. These may include missing permits, weak market evidence, unclear intellectual property rights, insufficient technical staff, unrealistic milestones or unconfirmed financing.

Common Reasons for Disqualification

The most common disqualifiers are:

-

Incorrect SME status after partner and linked enterprises are included.

-

Applicant type, legal form or company age does not match the call.

-

The project is implemented outside the eligible territory.

-

The sector or proposed activity is excluded.

-

The de minimis ceiling or another public aid limit is unavailable.

-

The project began before the permitted date.

-

The budget contains significant ineligible expenditure.

-

The company cannot prove co-financing or implementation capacity.

-

The applicant is an undertaking in difficulty or subject to a recovery order.

-

Required declarations or supporting documents are inaccurate or incomplete.

Some failures are absolute. Others can be corrected if discovered early.

A company may be able to restructure the budget, change the project timetable, clarify ownership relationships or resolve an administrative issue before submission. It cannot usually correct a missed deadline or reverse an investment that has already begun.

Early eligibility analysis is therefore more valuable than late proposal editing.

How a Grant Writer Can Conduct an Eligibility Review

A professional grant writer should not begin with the narrative section of the application.

The first task is to conduct an eligibility review.

This includes checking the company’s legal and SME status, ownership relationships, sector, location, project logic, costs, public aid history, implementation schedule and financial capacity.

The grant writer should also identify which conclusions require confirmation from an accountant, lawyer, public aid specialist, technical expert or programme operator.

A responsible adviser does not promise that a company “qualifies” after reading a programme headline. They distinguish between preliminary fit, confirmed eligibility and competitiveness.

For foreign founders, the review may also cover Polish registration, language requirements, accounting records, tax documents, signatures and the practical role of the Polish entity.

Platforms such as i-grants.com can support this process by connecting applicants with professionals who understand the relevant country, programme and funding rules. Structured applicant profiles can help grant writers assess company size, location, sector, project type and readiness before a full engagement begins.

The platform can also distinguish between an opportunity that appears relevant and one that has been verified against the official source.

Qualification Depends on the Entire Funding Structure

Qualifying for a small business grant in Poland involves much more than being a small company.

The applicant must meet the legal and organisational conditions. Its wider enterprise group must remain within the required size category. The project must be implemented in the correct territory and support the objective of the call. The budget must contain eligible costs. The public aid structure must comply with de minimis, aid intensity and cumulation rules. The company must also have the financial and operational capacity to complete the project.

A weakness in any one of these areas can make the application ineligible.

The safest approach is to perform the eligibility review before preparing the full proposal and before making binding project commitments.

A company qualifies for a Polish business grant only when the applicant, enterprise group, project, location, costs, financing structure and public aid position all meet the rules of the same call.

That is the difference between a company that looks suitable in a search result and an applicant that is genuinely ready to compete for funding.