French small and medium-sized enterprises have access to a broad range of public and public-backed financing instruments. Yet many business owners begin their search with only one question: “Which grant can we receive?”

That question is too narrow.

In France, a grant is only one part of the business funding system. Depending on the company’s size, location, project stage, financial capacity and sector, the most appropriate solution may be a grant, a repayable advance, a subsidised loan, a bank guarantee, a tax credit or an equity investment. In many cases, the strongest funding plan combines several instruments rather than relying on one source.

French public authorities officially recognise this diversity. Business support can take the form of direct aid, investment subsidies, subsidised loans, tax and social exemptions, repayment deferrals and other financing arrangements. The available support also depends heavily on the company’s location and the policies adopted by regional and local authorities.

For applicants, the practical challenge is therefore not simply to find public money. It is to identify the instrument that matches the company’s current stage, the risks of the project, the type of expenditure and the expected commercial outcome.

This guide explains the main funding instruments available to SMEs in France, how they differ and how businesses can build a realistic financing mix.

Why French SMEs need more than a grant search

France had approximately 5.18 million enterprises in the non-agricultural and non-financial market sectors in 2023. Almost 5 million were microenterprises, while approximately 174,600 were SMEs excluding microenterprises. Those SMEs employed around 4.64 million full-time equivalent workers and generated approximately 335.8 billion euros in value added.

These businesses do not have identical financing needs.

A young technology company may need funding for feasibility studies and prototype development before it generates revenue. A manufacturing SME may need several million euros for machinery and a new production line. A retailer may need a smaller investment to improve digital sales. An industrial company preparing an energy-efficiency project may first need a technical audit and then investment finance.

A single grant model cannot cover all these situations. This is why the French system uses different instruments for different levels of technical risk, commercial maturity and repayment capacity.

The main distinction is whether the support must be repaid.

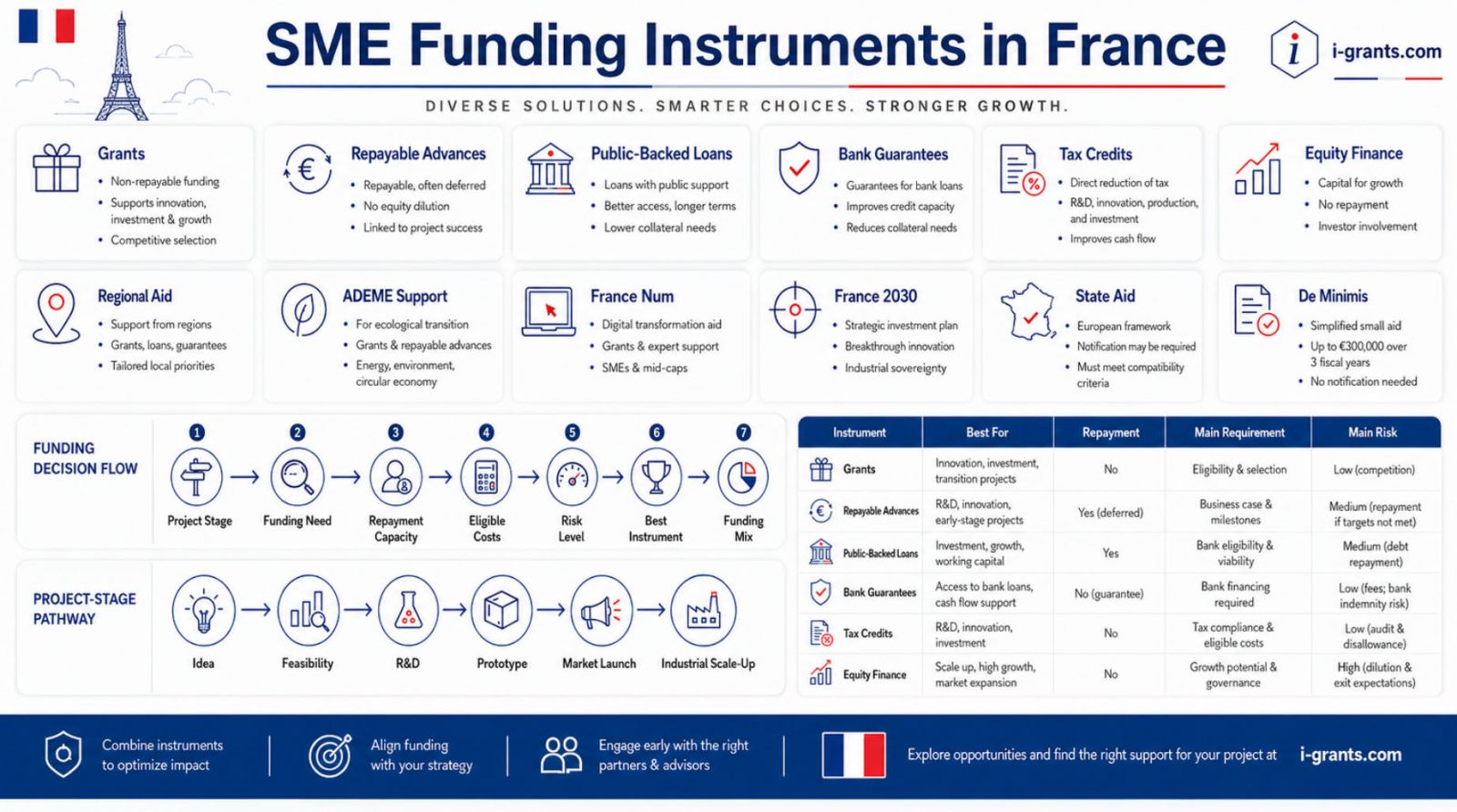

A grant normally covers part of eligible expenditure without repayment, provided that the beneficiary complies with the programme rules. A repayable advance must be returned according to the financing agreement. A loan creates a conventional repayment obligation. A guarantee does not provide cash directly but reduces the lender’s risk. A tax credit supports eligible expenditure through the tax system. Equity finance provides capital in exchange for an ownership interest or investment rights.

Table 1. Main SME funding instruments in France

| Instrument | How it works | Best suited to | Main limitation |

|---|---|---|---|

| Grant or investment subsidy | Covers part of eligible project expenditure without normal repayment | Innovation, ecological transition, regional investment, research, digitalisation | Usually requires co-financing and covers only approved costs |

| Repayable advance | Public financing repaid under agreed conditions, often without traditional collateral | Risky innovation projects with future commercial potential | Creates a future repayment obligation |

| Subsidised or public-backed loan | Provides debt financing under conditions designed for a target group or project | Business creation, equipment, expansion, market launch, digitalisation | The company must demonstrate repayment capacity |

| Bank guarantee | Covers part of the lender’s potential loss and facilitates access to credit | Companies with a viable project but limited collateral | Does not replace the bank’s credit assessment |

| Tax credit | Reduces tax due or creates a tax receivable based on eligible expenditure | Research, development, prototype design and innovation | Requires detailed technical and accounting evidence |

| Equity investment | Provides capital in return for shares or investment rights | High-growth startups, deep technology and scale-up projects | May dilute existing ownership and influence |

Grants and subsidies: valuable but rarely sufficient

Grants are attractive because they normally do not need to be repaid. However, they are rarely unrestricted payments that a business can use for any purpose.

Most French business grants are connected to a public policy objective. They may support research, technological development, ecological transition, industrial investment, digitalisation, exports, regional development or job creation. The project must fit that objective, and only costs defined as eligible in the programme rules can normally be included.

A grant may cover equipment, external expertise, research personnel, technical studies, prototypes, software or certain intangible assets. It may exclude normal salaries, rent, general marketing, working capital, loan repayments, recoverable value-added tax and expenditure incurred before the permitted project start date.

Grants also normally finance only a proportion of the project. The applicant must provide the remaining amount through its own resources, bank financing, investors or other compatible support. A company that wins a grant but cannot finance its share of the budget may still be unable to carry out the project.

Regional productive investment support illustrates this structure. The Région Sud programme for productive SME investments can support eligible expenditure at rates that may range from 10 to 20 percent under one SME aid framework and from 25 to 35 percent under certain regional aid conditions. The rate depends on factors such as company size, location and the applicable state-aid basis.

This means that the company still needs to finance most of the project. A 20 percent subsidy for a 500,000-euro investment does not eliminate the need to secure the other 400,000 euros.

Applicants should therefore evaluate a grant as one layer of the financing plan, not as the complete plan.

Repayable advances: public support that must be returned

Repayable advances are common in French innovation financing. They are particularly useful when a project is too risky for a conventional bank loan but has a reasonable possibility of generating commercial income.

Bpifrance Création describes a repayable advance as a zero-interest, non-bank loan used to finance certain business expenditure, generally connected with development, research or innovation. It is normally granted by the state or a territorial authority through a specific financing scheme and may be provided without traditional guarantees.

The exact repayment conditions vary. Some programmes establish a fixed schedule. Others may link part of the repayment to the technical or commercial outcome of the project. The funding agreement must always be reviewed carefully.

The main benefit is that the company obtains early financing without immediately using conventional bank debt or giving up equity. The main disadvantage is that the support is not free. If the project proceeds successfully, the company must plan for future repayments.

Some Bpifrance innovation support combines a grant and a repayable advance. The Aide pour le développement de l’innovation, for example, can take the form of a mixed grant and recoverable advance, with total support reaching up to 2 million euros for programmes lasting no more than 36 months. Expenditure committed before the application date is not eligible.

This mixed structure is logical. The grant component absorbs part of the high technical risk, while the repayable component allows public funds to be recycled if the project advances.

For SMEs, repayable advances are often more appropriate than grants when the project has a clear route to market but still involves substantial uncertainty.

Loans: financing growth beyond the grant stage

Loans become more relevant when an enterprise has moved beyond early research and can demonstrate a credible business model, repayment capacity or market demand.

Bpifrance describes its financing offer as covering companies from initial development to stock-market listing, using instruments ranging from credit to equity. Bpifrance Création also explains that innovative projects require different financing at different stages. Own resources and early public aid may support feasibility work, while grants, repayable advances and tax measures can support research and development. Loans, banks and investors become increasingly important during market launch and growth.

A public-backed or subsidised loan may offer advantages such as a repayment holiday, no personal guarantee, a longer term or eligibility for expenditure that a grant would not cover. However, it remains debt. The company must show that future cash flow can support repayment.

Digital transformation provides a useful current example. The Bpifrance Flash Prêt Boost - Transformation numérique is designed for businesses that have operated for more than three years and employ between 2 and 49 people. It can provide between 5,000 and 75,000 euros over three to five years, without a personal guarantee, with a possible repayment deferral of 9 to 12 months.

A similar Prêt Boost for electronic invoicing was listed in 2026 for eligible TPEs and SMEs preparing for France’s electronic invoicing reform. It offered between 5,000 and 75,000 euros without a guarantee, with repayment over three to five years and a possible deferral.

These instruments demonstrate an important principle: even when public policy encourages a business transition, support may be provided as a loan rather than a grant.

Guarantees: solving the collateral problem

Some viable SMEs do not need a subsidy. They need a bank to approve a loan.

The problem may be limited collateral, a short trading history, a business acquisition, an innovation risk or a large investment relative to the company’s existing balance sheet. In these situations, a guarantee can be more useful than a small grant.

A guarantee covers part of the lender’s potential loss if the borrower defaults. Bpifrance officially guarantees loans made to enterprises by French banks in order to encourage financing of projects considered more risky.

The guarantee does not mean that the bank has no risk. Bpifrance describes the mechanism as a sharing of the final loss with the bank, while the bank retains its own portion of the risk.

For example, the Bpifrance standard creation guarantee can cover up to 60 percent of certain loans provided to eligible SMEs less than three years old. Covered financing may include tangible and intangible investments, the purchase of a business, working capital needs and some company acquisition transactions.

A guarantee can therefore make a credit application more acceptable, but it does not replace normal underwriting. The bank will still assess the company’s business plan, repayment capacity, management, accounts and financial forecasts.

From the applicant’s perspective, the correct question is not “Can we obtain a guarantee instead of repaying the loan?” It is “Can risk sharing help the bank finance an otherwise credible project?”

Tax credits: financing through the tax system

Tax credits are among the most important forms of innovation support in France. They differ fundamentally from grants because the company normally claims them through its tax reporting rather than through a conventional competitive grant call.

The Crédit d’impôt recherche, commonly known as CIR, encourages companies to undertake research and development. Eligible expenditure can include specific personnel, equipment, subcontracted research and other qualifying research costs, subject to detailed rules.

The Crédit d’impôt innovation, or CII, is an extension intended for SMEs carrying out certain innovation activities. It applies to eligible expenditure incurred up to 31 December 2027 and focuses on the design of prototypes or pilot installations for new products.

The expenditure base used to calculate the CII is capped at 400,000 euros. As currently presented by Service Public, the credit rate is 20 percent in metropolitan France, with different rates in overseas departments and Corsica. Public subsidies received for the same research or innovation project must be deducted from the expenditure used to calculate the credit, and costs already included in the CIR cannot also be included in the CII.

This shows why applicants need an integrated funding calculation. A company cannot simply add a grant, CII and CIR as if each instrument applied independently to the full cost base.

Tax credits also create a documentation risk. The company must be able to explain why the work qualifies as research or innovation, which staff worked on it, how working time was calculated, which subcontractors were used and how expenditure was recorded.

For technically complex projects, the tax file should be treated with the same discipline as a grant application.

Equity, quasi-equity and loans of honour

Some projects need capital rather than public aid.

High-growth startups, deep-technology companies and businesses planning rapid expansion may require equity because they cannot safely repay large loans during their early years. Equity investors accept higher risk in exchange for shares and the possibility of future growth.

Bpifrance supports equity investment directly and indirectly, often alongside other market investors, to finance companies with strong growth potential.

For smaller creation and takeover projects, a loan of honour can strengthen the founder’s financial position. These loans are generally provided at zero interest without a personal guarantee or collateral and may include a repayment deferral. According to figures cited by Bpifrance Création, one euro of a loan of honour is associated on average with 9.5 euros of complementary bank financing through Initiative France and 13 euros through Réseau Entreprendre.

A loan of honour is granted to the individual founder, while a repayable advance is normally granted to the enterprise. The two instruments should not be confused.

Equity and quasi-equity are particularly relevant when the main financing problem is insufficient capital rather than a lack of eligible grant expenditure.

Matching the instrument to the project stage

The same company may need several funding instruments over the life of one project.

An early feasibility study may be supported by a small grant or diagnostic programme. Research and prototype development may use a grant, repayable advance, CIR or CII. Industrialisation may require equipment finance, regional investment aid and a bank loan. Commercial launch may require working capital, a guarantee or investors.

This progression is especially visible in innovation funding. Early public support often absorbs technical uncertainty. Debt becomes more suitable when the company can show commercial prospects. Equity becomes important when rapid growth requires substantial capital but repayment capacity remains limited.

Table 2. Choosing a French SME funding instrument by project situation

| Project situation | Most relevant instruments | Why they may fit | Critical checks |

|---|---|---|---|

| Early idea or feasibility study | Small grant, diagnostic support, competition, own resources | The project is not yet ready for conventional debt | Technical novelty, project scope, initial evidence |

| Research and prototype development | Grant, repayable advance, CIR, CII | Technical risk is high and revenue may still be distant | Research documentation, staff costs, subcontractors, start date |

| Market launch | Innovation loan, bank loan, guarantee, equity | The project has a commercial plan but needs launch capital | Sales assumptions, repayment capacity, working capital |

| Productive investment | Regional subsidy, FEDER support, equipment loan, guarantee | The project may create production capacity and employment | Location, eligible equipment, aid intensity, co-financing |

| Ecological transition | ADEME study support, investment grant, green loan | Technical assessment may be needed before investment | Environmental baseline, energy savings, emissions and additional cost |

| Digital transformation | Regional digital aid, France Num support, public-backed loan | Projects vary from small software investments to process reform | Supplier scope, cyber security, implementation capacity |

| Limited collateral | Bpifrance or regional guarantee, bank loan | The business case may be sound even when collateral is weak | Bankability, financial forecasts, retained lender risk |

| Rapid scale-up | Equity, quasi-equity, France 2030, innovation finance | High capital needs may exceed safe borrowing capacity | Growth strategy, ownership dilution, governance and exit expectations |

Regional funding can change the answer

France’s regional structure means that two similar SMEs may have access to different instruments depending on where their project is carried out.

Regional authorities can offer investment grants, innovation support, digital vouchers, loans, guarantees and support funded through the European Regional Development Fund. Local economic priorities influence which sectors, territories and costs receive support.

Innov’up in Île-de-France is an example of a programme that can support research, development and innovation through grants and repayable finance. The programme has historically allowed support of up to 500,000 euros as a grant and up to 3 million euros as a repayable advance, depending on the project and assessment.

The Région Sud productive investment programme supports SMEs developing new processes while maintaining or creating employment. Its current deadline is listed as 31 December 2029, and the level of support depends on the applicable regional and SME state-aid framework.

Applicants should therefore search by project location, not only by the address of the company’s registered office. A regional programme may require the investment, jobs and economic impact to occur within the region.

ADEME funding for ecological transition

ADEME is a central public actor for business projects connected with energy, circular economy, decarbonisation, waste, sustainable production and other environmental priorities.

Its enterprise platform includes grants, calls for projects, diagnostics and studies offered by ADEME and other public organisations such as chambers of commerce, chambers of trades and regional authorities.

The form of support depends on the stage of the environmental project. A company may first receive help for an audit or feasibility study and later apply for investment support. Some projects are evaluated according to the additional cost of the environmentally preferable solution compared with a conventional alternative.

For example, an ADEME ecodesign investment scheme published for 2026 stated that support could range from 15 to 60 percent depending on the project and company size. It also referred to the calculation of additional costs and to state-aid frameworks such as the General Block Exemption Regulation or de minimis rules.

This means that companies should not begin an ecological funding search by asking only how much their equipment costs. They should establish the environmental baseline, expected energy or material savings, emissions impact and additional cost compared with the normal investment scenario.

France Num and digital investment

France Num is the French public initiative supporting the digital transformation of TPEs and SMEs. Its resources cover digital strategy, cyber security, artificial intelligence, production, commercial development and financial support.

Digital support varies significantly by region. Some authorities provide small subsidies for software, cyber security, online sales or digital equipment. Other needs are addressed through loans, diagnostics or expert support.

As of July 2026, the France Num financial aid database displayed more than 300 entries, including regional grants, loans and other support instruments. Because these programmes change regularly, applicants should verify the current deadline, territory, beneficiary definition and eligible expenditure before preparing an application.

France 2030: strategic funding rather than a general SME grant

France 2030 should not be treated as a general source of small grants for ordinary business expenditure.

It is a strategic investment framework focused on innovation, industrial transformation, future technologies and decarbonisation. Calls may support research, demonstration, first industrial deployment, strategic manufacturing or the development of technologies considered important for France’s future economy.

For SMEs, France 2030 is most relevant when a project has substantial innovation, industrial or strategic value. A routine website, replacement vehicle or standard equipment purchase is unlikely to fit simply because the applicant is an SME.

The company must normally demonstrate more than financial need. It may need to show technological advancement, market potential, industrial impact, environmental benefits, partnerships, intellectual property, execution capacity and a credible financing plan.

State aid, de minimis and cumulation

The choice of instrument cannot be separated from EU state-aid rules.

Under the general de minimis regulation, a Member State cannot provide more than 300,000 euros in de minimis aid over three years to a single undertaking. The term “single undertaking” includes the recipient and relevant linked enterprises.

France created a national State Aid Platform to record de minimis aid, following the requirement for Member States to establish a central register from 1 January 2026. The aim is to reduce administrative burden and help prevent companies from exceeding the applicable limits.

Companies should nevertheless maintain their own aid register. It should identify the beneficiary entity, granting authority, decision date, amount, legal basis, gross grant equivalent and expenditure covered.

Cumulation must also be checked at cost level. A regional grant, tax credit and subsidised loan may sometimes be combined, but the company cannot assume that each can be calculated on the same full expenditure. Public subsidies may need to be deducted before calculating a tax credit, and total aid intensity may be capped.

The project start rule is equally important. Many aid schemes require the application to be submitted before the company enters into a binding commitment. Signing an equipment order or paying a deposit too early may make the project or expenditure ineligible.

How to build a realistic funding mix

A strong French SME funding plan begins with the complete project budget, not with a list of available grants.

The company should separate technical development, equipment, external services, staff, intellectual property, market launch, working capital and non-eligible operating expenditure. It should then assign the most appropriate source to each cost category.

For example, a manufacturing innovation project might use a grant for technical development, CII or CIR for eligible innovation work, a regional subsidy for equipment, a bank loan supported by a guarantee for the remaining investment and equity for working capital and commercial expansion.

This approach has several advantages. It avoids asking one programme to finance costs outside its purpose. It demonstrates co-financing capacity. It reduces dependence on a single decision. It also allows the company to match short-term and long-term financing with the economic life of the expenditure.

However, the mix must remain manageable. Too many instruments can create overlapping reporting duties, incompatible start dates, different eligible cost rules and cumulation risks.

Pre-application funding checklist

Before choosing or combining French SME financing instruments, the company should confirm:

-

The current project stage, from feasibility and research to industrial investment, market launch or expansion.

-

The exact funding gap and whether it concerns technical risk, equipment, working capital, collateral or capital.

-

The costs that are eligible for public aid and those that must be financed commercially.

-

The amount of own funding and co-financing available.

-

The company’s capacity to repay loans or repayable advances.

-

Whether any contract, order, deposit or binding commitment has already started the project.

-

Previous de minimis and other state aid received by the applicant and linked companies.

-

The regional, sectoral, environmental and company-size conditions of each instrument.

-

The interaction between grants, tax credits, guarantees and loans.

-

The financial statements, forecasts, quotations, technical evidence and project schedule required for assessment.

When an SME should hire a grant writer or funding adviser

A professional grant writer can add value before any application is drafted.

The first task should be to diagnose the financing need. A company that asks for a grant may actually need a bank guarantee. A startup seeking a loan may need more equity first. An innovation project may be better served by a combination of a repayable advance and tax credit. An environmental investment may require an audit before an equipment application is possible.

A qualified adviser can map the project stage, identify eligible costs, compare national and regional programmes, review state-aid exposure and develop a financing structure that remains realistic even if one application is unsuccessful.

Through i-grants.com, SMEs can connect with grant writers and public funding specialists who understand particular French programmes, regions and sectors. The most useful professional is not the person who promises the largest grant. It is the person who can explain which instruments fit the project, which costs qualify, what the company must finance itself and which risks could prevent approval.

Conclusion

France offers SMEs much more than conventional grants. Its financing system includes subsidies, repayable advances, public-backed loans, guarantees, tax credits, regional instruments, environmental support and equity finance.

Each instrument solves a different problem.

Grants can absorb part of the cost of projects that serve a public objective. Repayable advances can support risky innovation before normal debt becomes realistic. Loans finance investments that can generate enough cash for repayment. Guarantees help viable businesses overcome collateral gaps. Tax credits reward eligible research and innovation expenditure. Equity supports companies that need patient capital for rapid growth.

The strongest applicants do not build a grant wish list. They build a financing architecture.

For a French SME, the right strategy is to define the project, separate eligible and non-eligible expenditure, determine the company’s repayment and co-financing capacity, review state-aid limits and then match each financing need with the appropriate instrument. That approach produces a more credible application, a more resilient budget and a better chance of completing the project successfully.